Key Takeaways

- Breathe first: You do not have to make any big moves with your money today or even this month. Putting your inheritance into a safe holding zone gives you time to think clearly.

- Build your squad: Gathering trusted professionals like a certified financial planner and a tax expert helps you avoid costly money mistakes.

- Map your goals: Divide your inheritance into three main categories: paying off high-interest debt, saving for your future, and enjoying a small part of it now.

- Understand the tax rules: Different types of inherited assets carry different tax burdens, so knowing what you own helps you keep more of it.

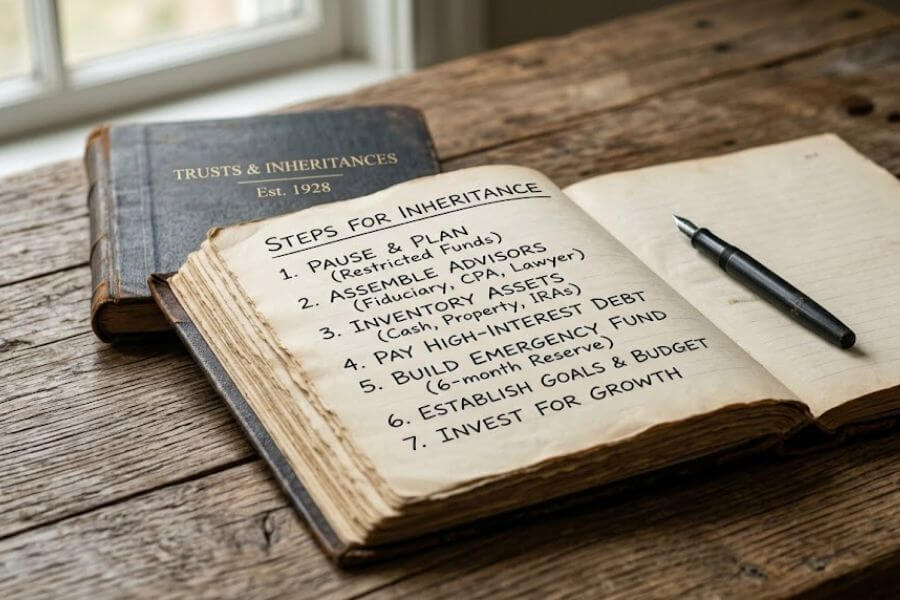

The First Step is to Take a Deep Breath

Receiving an inheritance brings up a flood of mixed feelings. You might feel deeply sad about losing someone you love, while also feeling surprised by a sudden influx of cash. It is completely normal to feel overwhelmed, confused, or even a bit guilty. The most important thing you can do right now is absolutely nothing. You do not need to rush out and buy a new car, quit your job, or invest in the stock market tomorrow.

Many people make the mistake of rushing into big decisions while their emotions are running high. Instead, give yourself permission to pause. Call a time-out on any major lifestyle changes. By setting the money aside in a secure place for a few months, you create a buffer between your grief and your long-term financial choices. This simple pause ensures that whatever you choose to do next comes from a place of logic and calm, rather than impulse or stress.

Create Your Temporary Money Safe Zone

Before you can build a permanent plan for your wealth, you need to put it somewhere secure. You want a financial institution where your money can earn a little bit of interest without any risk of losing its value. This is your temporary holding tank while you sort out the details.

High-Yield Savings Accounts

A high-yield savings account is an excellent spot for cash. These accounts are offered by many traditional banks and online financial companies. They pay a much higher interest rate than a standard checking account, which means your money grows slightly while it sits there. The best part is that you can withdraw the cash whenever you are ready to use it.

Certificates of Deposit

If you know you will not need to touch the money for six months or a year, a certificate of deposit is another strong option. You agree to leave your money with the bank for a set period, and in exchange, they give you a guaranteed interest rate. This prevents you from spending the money on a whim since taking it out early usually results in a small penalty.

Treasury Bills

For larger amounts of money, some people look at short-term government bonds. These are backed by the federal government, making them incredibly secure. They pay out after a few weeks or months, giving you a steady place to park your cash while you interview financial professionals and weigh your choices.

Assemble Your Financial Dream Team

Managing a large amount of wealth is rarely a solo project. Trying to figure out tax laws, investment strategies, and estate planning by yourself can quickly lead to burnout. Building a team of experts ensures that you protect your new wealth and maximize its growth.

Certified Financial Planner

A certified financial planner acts like the head coach of your team. They look at your entire life picture, including your career goals, family situation, and retirement dreams, to build a customized roadmap for your money. Look for a professional who acts as a fiduciary, which means they are legally required to put your best interests ahead of their own profits.

Certified Public Accountant

Taxes can eat away a huge chunk of your inheritance if you are not careful. A certified public accountant helps you understand the exact tax rules tied to the assets you received. They find legal ways to reduce what you owe to the government, ensuring that the majority of the money stays in your hands.

Estate Planning Attorney

If your inheritance includes complicated pieces like a family trust, real estate properties, or a business, you will want an attorney on your side. They handle the legal paperwork, help transfer titles into your name, and ensure that everything moves forward according to the law.

Team Member Roles and Selection Tips

| Specialist | Main Responsibility | What to Look For |

| Financial Planner | Creates your overall wealth roadmap | Fiduciary status and fee-only pay structure |

| Tax Professional | Lowers your tax burden on the wealth | Deep experience with inherited assets |

| Estate Attorney | Handles deeds, trusts, and legal titles | Local expertise in your specific state laws |

Inventory and Understand Your Inheritance

Not all inheritances are created equal. Receiving a box of cash is very different from inheriting a house, a stock portfolio, or a retirement account. To make smart choices, you must categorize exactly what you have been given.

Cash and Liquid Bank Accounts

This is the most straightforward asset to manage. It includes checking accounts, savings accounts, and physical money. Once the legal probate process wraps up, this money transfers directly to you, and you can move it into your temporary safe zone right away.

Retirement Accounts

Inheriting a retirement account like a traditional IRA or a 404k comes with very specific government rules. In many cases, the law requires you to withdraw all the money from the account within ten years. Because these withdrawals can count as income, they might bump you into a higher tax bracket if you take out too much at once.

Stocks, Bonds, and Mutual Funds

If you inherit a portfolio of investments, you generally receive a step-up in basis. This means the value of the stocks is reset to what they were worth on the day your loved one passed away, rather than what they paid for them decades ago. This rule can save you thousands of dollars in capital gains taxes if you choose to sell the investments immediately.

Real Estate and Physical Property

Inheriting a home, a piece of land, or a commercial building introduces regular ongoing costs. You are now responsible for property taxes, homeowners insurance, monthly utilities, and general repairs. You need to decide quickly whether you want to move into the property, turn it into a rental unit, or sell it on the open market.

Clear Away Your Financial Obstacles

Once your money is secure and you have an understanding of what you own, it is time to use a portion of it to clean up your current financial life. The fastest way to guarantee a massive return on your money is to eliminate your high-interest liabilities.

Tackle High-Interest Debt First

Credit card debt, personal loans, and high-interest car payments act like financial anchors holding you back. If you are paying fifteen or twenty percent interest on a credit card balance, using your inheritance to wipe that balance to zero is the smartest move you can make. It instantly frees up your monthly cash flow and stops you from throwing money away on interest fees.

Evaluate Low-Interest Loans Carefully

Not all debt needs to be wiped out immediately. Mortgages or student loans with very low interest rates might not be worth paying off right away. If your mortgage interest rate is three percent, but you can safely earn five percent on your savings, it makes more sense to keep making your regular monthly payments and invest the extra cash elsewhere.

Debt Payoff Priority List

- Priority One: Credit card balances and payday loans (usually fifteen percent interest or higher).

- Priority Two: Personal loans and high-rate auto financing (between eight and fourteen percent interest).

- Priority Three: Private student loans with variable rates.

- Priority Four: Low-interest federal student loans and fixed-rate home mortgages.

Establish a Rock-Solid Emergency Fund

Life is unpredictable, and emergencies always seem to happen at the worst possible times. Before you look at long-term investing, use a slice of your inheritance to build an emergency fund that protects you from future financial stress.

How Much Do You Really Need?

A standard emergency fund should cover three to six months of your essential living expenses. This includes your rent or mortgage, groceries, utilities, insurance, and minimum loan payments. If you work in a volatile industry or run your own business, aiming for a full year of expenses provides an extra layer of comfort.

Keep It Separate and Accessible

Your emergency fund should live in a high-yield savings account completely separate from your everyday spending cash. You do not want to see this balance when you log in to buy groceries or shop online. It should only be touched for true emergencies, like an unexpected medical bill, a major car breakdown, or a sudden job loss.

Define Your Personal and Financial Goals

Money is simply a tool that helps you live the life you want. Now that your debts are handled and your emergency fund is full, you can dream about what you want your future to look like. Sit down with a notebook and write out your short-term, medium-term, and long-term milestones.

Short-Term Targets (One to Three Years)

These are goals you want to hit in the near future. It could mean going back to school to finish a degree, taking a meaningful family vacation to honor the person who passed away, or buying a dependable vehicle. Because you need this cash soon, keep it out of volatile investments like individual stocks.

Medium-Term Goals (Three to Ten Years)

Medium-term milestones require a bit more patience. Examples include saving up a massive down payment for a suburban home, gathering the seed money to launch your own business, or starting a college fund for your young children. You can take a moderate amount of risk with this money to help it grow.

Long-Term Dreams (Ten Years or More)

Long-term planning is almost always focused on achieving complete financial independence and a comfortable retirement. This is money you will not touch for decades, meaning you can ride out the natural ups and downs of the stock market to build significant wealth over time.

Master the Basics of Investing Your Wealth

Investing can feel like learning a foreign language, but the core principles are straightforward. The goal is to put your money into assets that increase in value over time, outrunning inflation and building true wealth.

The Power of Compound Interest

Compound interest happens when your money earns interest, and then that interest earns interest of its own. Over a long period, this creates a snowball effect where your wealth grows faster and faster without you adding another single penny to it. Starting early gives your money more time to compound.

Diversification is Your Best Friend

Never put all your eggs into one single basket. If you invest your entire inheritance into one popular tech stock and that company goes bankrupt, your wealth vanishes. Instead, spread your money across hundreds of different companies through index funds and mutual funds. If a few companies struggle, the others help pick up the slack.

Asset Allocation Explained

Asset allocation is the mix of different investment types you hold in your portfolio. The two main categories are stocks and bonds. Stocks represent ownership in companies and offer high growth potential with higher risk. Bonds are essentially loans to corporations or governments that provide steady, lower-risk returns.

Investment Type Comparison

| Investment Category | Risk Level | Growth Potential | Main Purpose |

| Single Stocks | Very High | Massive | Speculation and rapid growth |

| Index Funds | Moderate | High | Long-term wealth building |

| Corporate Bonds | Low | Conservative | Income and stability |

| Cash Savings | None | Minimal | Safety and quick access |

Navigate the Complex World of Real Estate

If your inheritance includes a home or land, or if you plan to use cash to buy property, you need to weigh the pros and cons carefully. Real estate can be a wonderful wealth-builder, but it also demands regular time, effort, and cash.

Keeping the Inherited Family Home

Deciding to move into a house passed down by a parent or relative is deeply emotional. You must look past the memories and inspect the actual physical structure. Can you comfortably afford the yearly property taxes? Is the roof about to leak? If the house requires massive upgrades that drain your savings, selling it might be the healthier choice for your wallet.

Becoming a Landlord

Turning an inherited property into a rental unit sounds like a great way to earn passive income, but managing tenants is hard work. You will have to handle middle-of-the-night maintenance emergencies, repair damage between renters, and deal with empty months where no rent is coming in. If you do not want that stress, you can hire a property management company, though they will take a percentage of your monthly profit.

Selling the Property for Cash

Selling the home allows you to split the proceeds cleanly if you share the inheritance with siblings. It frees you from ongoing maintenance worries and lets you reallocate that wealth into a diversified investment portfolio that does not require any physical labor or upkeep.

Handle the Emotional Side of Windfall Wealth

Sudden wealth syndrome is a real psychological condition that affects people who inherit large amounts of money quickly. It can lead to anxiety, confusion, and a strange sense of isolation from friends and family members who do not have the same financial security.

Managing the Guilt of Inheriting

It is common to feel uncomfortable enjoying money that came because someone you love passed away. You might feel like you did not earn it, or that spending it is disrespectful. Remember that your loved one worked hard and chose to leave this legacy to you because they wanted to make your life more comfortable and secure. Using the money wisely is the ultimate way to honor their memory.

Dealing with Sudden Requests for Money

When word gets out that you inherited a significant sum, distant relatives or old acquaintances might suddenly appear with business ideas, investment pitches, or personal sob stories asking for financial help. It can be incredibly painful to say no to people you care about.

How to Say No Gracefully

- Use your professional team as a shield by saying, “My financial planner has locked up the funds in a long-term investment plan, so I do not have access to extra cash right now.”

- Set a firm boundary early by telling family members, “I have made a strict rule not to mix my personal relationships with financial loans or business investments.”

- Keep your inheritance details private, sharing the exact numbers only with your spouse and your professional advisors.

Give Yourself Permission to Enjoy a Small Portion

While saving and investing for your future is incredibly important, you do not need to be a financial robot. It is completely healthy to take a small, reasonable percentage of your inheritance and use it to bring joy to your life right now.

The Five Percent Rule

Many financial experts recommend taking around five percent of the total inheritance and putting it into a fun bucket. If you inherit one hundred thousand dollars, taking five thousand dollars to go on a memorable vacation, upgrade an old appliance, or buy a favorite piece of artwork is a great choice.

This small reward satisfies your immediate desires and makes it much easier to stay disciplined with the remaining ninety-five percent of the money. It honors the spirit of the gift while protecting the vast majority of your financial future.

Plan for Your Own Legacy and Future

Receiving an inheritance often shifts your perspective on life. It forces you to realize that wealth passes from one generation to the next, and it gives you the rare opportunity to think about what kind of mark you want to leave on the world.

Updating Your Own Estate Plan

Now that your net worth has increased, your old legal documents might be outdated. You need to write or revise your own will, update the beneficiary designations on your bank and retirement accounts, and establish medical powers of attorney. This ensures that if anything ever happens to you, your assets will protect your children or favorite causes without passing through a messy legal battle.

Exploring Charitable Giving

If you find yourself with more money than you realistically need to reach your personal goals, you might consider philanthropy. You can set up a charitable donor-advised fund, make direct donations to local non-profit organizations, or establish a small scholarship fund at your former school. Giving back allows you to turn your inheritance into a permanent force for good in your community.

Step-by-Step Action Roadmap

To make sure you do not feel overwhelmed, break down the entire inheritance process into specific phases based on time.

Days One through Thirty: The Boundary Phase

- Focus entirely on your emotional well-being and supporting your family through grief.

- Do not make any major purchases, career alterations, or permanent investment moves.

- Open a secure, high-yield savings account and place any immediate cash distributions there.

Months Two through Six: The Discovery Phase

- Gather all legal documents, account statements, and property deeds related to the estate.

- Interview and hire your professional team, starting with a certified financial planner and a tax accountant.

- Review your current personal finances, tracking down all outstanding credit balances and monthly living expenses.

Months Six through Twelve: The Execution Phase

- Wipe out your high-interest credit cards and personal loans completely.

- Fill your emergency fund until it holds at least six months of living expenses.

- Build a diversified investment portfolio aligned with your long-term retirement milestones.

- Set aside your small fun budget and use it to celebrate the memory of your loved one.

Frequently Asked Questions

What should I do first when I learn I am getting an inheritance?

The very first move is to pause and avoid making any impulsive choices. Do not buy expensive items, quit your current employment, or promise financial gifts to anyone else. Put the funds into a safe, insured bank account where it can sit securely while you process your emotions and build a qualified team of professionals to guide you.

Will I have to pay heavy taxes on the money I inherit?

In the United States, there is no federal inheritance tax on individual recipients, though a handful of states do collect their own version. However, if you inherit a traditional retirement account, you will owe regular income taxes as you withdraw the money. Inheriting stocks or property usually grants you a reset value, which eliminates taxes on past growth.

Should I use my inheritance to pay off my home mortgage immediately?

It depends entirely on your mortgage interest rate and your overall financial picture. If your home loan has a very low fixed interest rate, you are often better off keeping the mortgage and investing your inheritance in a diversified portfolio that earns a higher return. If your mortgage rate is high or you value the peace of mind of owning your home free and clear, paying it off can be a great option.

How do I handle friends and family members who ask for a loan?

The cleanest approach is to create a firm boundary and blame your professional team. Tell them that your money is locked into a strict, long-term plan managed by your financial advisor and that you cannot pull out cash for personal loans. This keeps your personal relationships healthy while protecting your wealth from burning away.

Is it okay to spend some of the inheritance cash on fun things right away?

Yes, it is perfectly fine to enjoy a small portion of the money, as long as it is done intentionally. A great strategy is to follow the five percent rule, dedicating a tiny fraction of the total windfall to a vacation or a special purchase, while directing the remaining balance toward your long-term safety, debt elimination, and retirement goals.

{kind=link}